NSW floods expose a deeper crisis: the shrinking reach of affordable insurance

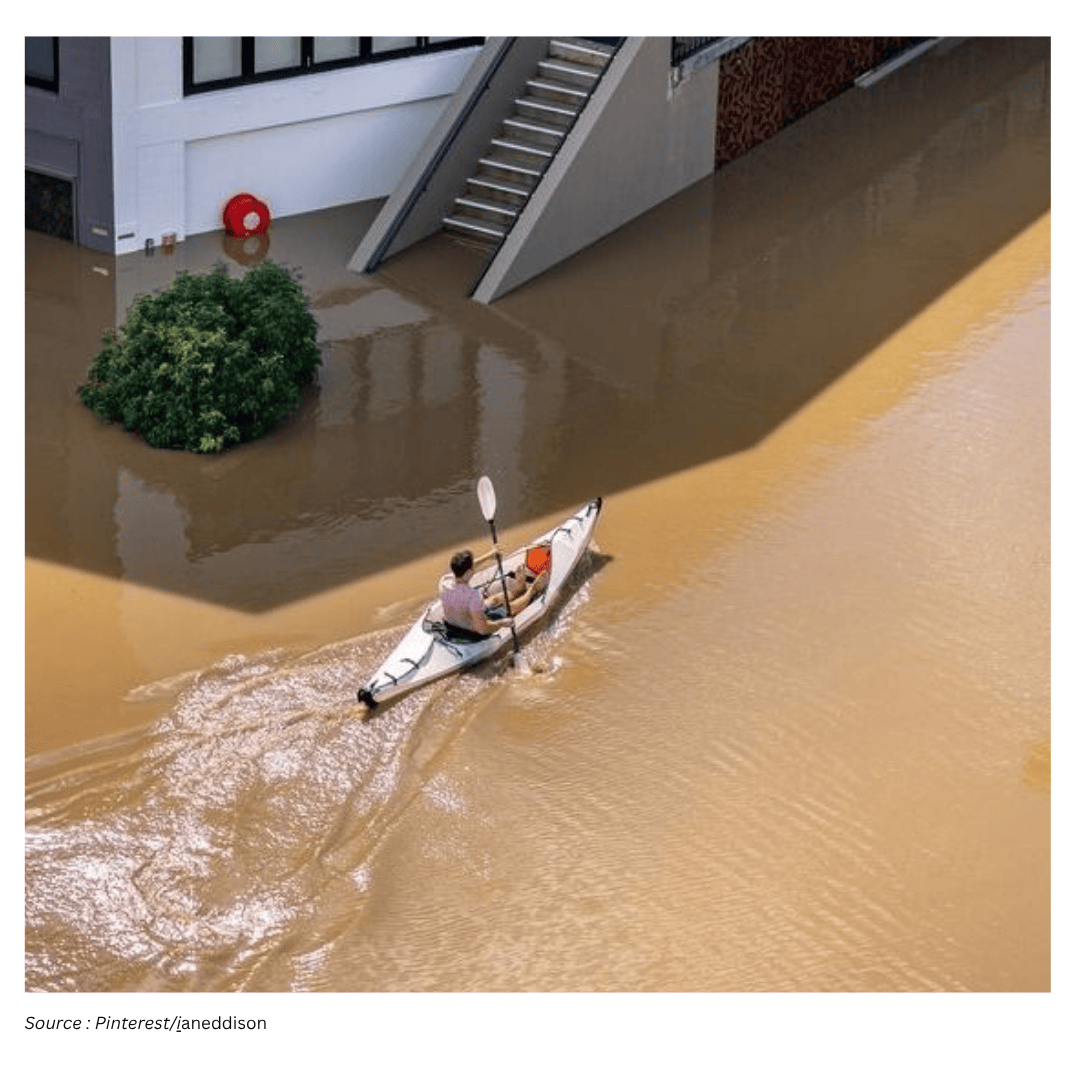

Large parts of New South Wales have again been devastated by floods, with early estimates suggesting about 10,000 homes and businesses may have been damaged or destroyed. The Insurance Council of Australia has reported more than 6,000 insurance claims lodged for the Mid North Coast and Hunter region. Hundreds of families are displaced, and with many properties now uninhabitable, the immediate challenge of clean-up is quickly giving way to a longer, more uncertain question: what happens when insurance is unavailable, unaffordable, or insufficient?

This is not simply a story about how quickly insurers process claims after a disaster. It is increasingly a story about whether households, businesses and communities can secure meaningful protection at all. In the aftermath of the NSW floods, accounts are emerging of people without cover and of residents saying premiums were quoted as high as A$30,000 a year. Many others are underinsured, finding that payouts do not meet the full costs of rebuilding, repair and replacement. The Insurance Council of Australia has declared the event an “insurance catastrophe”, a label that captures the scale of claims but also hints at the stress building across the system.

A local disaster with global echoes

The NSW floods are part of a wider pattern. In 2024, around 60 natural disaster events each exceeded A$1.5 billion in economic losses, and total losses worldwide reached A$650 billion. These figures underline why the debate about insurance is no longer confined to individual policies or single events. As disasters escalate in a changing climate, the question becomes structural: are we moving toward a future where insurability itself erodes for large parts of the population?

Australia is among the most disaster-prone countries in the Western world. That reality has led to a stark framing: is Australia becoming the “canary in the coalmine” for a global collapse of insurance? With repeated disasters and rising costs, it is understandable that people feel, and fear, that this is already happening.

The idea of an uninsurable future is not new

The prospect that climate-related risks could overwhelm private insurance has been debated for decades. In 1992, sociologist Ulrich Beck argued that unpredictable global risks, including climate change, would bring an end to the private insurance market, with profound effects on modern life. The concept of an “uninsurable future” can easily conjure dramatic images—crumbling buildings and communities struggling amid ruins.

Yet the more immediate point is less cinematic and more practical: for many people, the collapse is not a future event. It is already unfolding through affordability and availability. The experience of households and businesses in flood-affected parts of NSW—those without cover, those priced out, and those whose policies fall short—illustrates how this shift can take hold gradually, policy by policy, renewal by renewal.

Political pressure meets market realities

In the days after the floods, NSW Premier Chris Minns said he would be “putting the heat” on insurance companies, arguing that “everyone’s going to have to do their part” and that insurers must “step up and pay out claims quickly.” In the lead-up to the federal election, both major parties also signalled they believed insurers were “ripping off” Australians. The Coalition went further, proposing new emergency divestiture powers that would allow government to break up major insurers in the event of market failure.

But the forces shaping insurance pricing and coverage do not stop at the domestic market. A central constraint is that insurance is heavily influenced by global “reinsurers”—companies that provide insurance for insurers, helping cover the cost of paying out claims after major disasters. This matters because the cost and availability of reinsurance can flow through to premiums and underwriting decisions at the retail level.

Market concentration is also part of the picture. Just ten multi-billion-dollar companies control 70% of the reinsurance market. When a small number of global firms dominate such a critical layer of the system, local political pressure on retail insurers may have limited reach, especially when risk is rising and large losses are becoming more frequent.

Who bears the burden when cover shrinks?

While public debate often focuses on insurers’ financial health, the more pressing issue described by observers of the current crisis is the “real-time collapse of insurance for households, businesses and communities.” In practical terms, this collapse can look like:

People being unable to obtain cover at all in high-risk areas.

Premiums rising to levels that households and small businesses cannot sustain.

Underinsurance, where policies exist but payouts do not cover the true cost of rebuilding, repair and replacement.

Communities facing repeated disasters while the financial tools meant to spread risk become less accessible.

The consequences are especially severe for those already struggling to make ends meet. When insurance becomes a luxury rather than a baseline safeguard, disasters can deepen hardship and widen inequality. After a flood, a household without adequate cover may face not only the loss of a home or possessions, but also the prospect of prolonged displacement and financial instability.

Rising costs across multiple types of insurance

The pressure is not limited to flood cover. In places like Australia, increasing insurance costs are cutting across multiple categories, with the largest rises reported in home, vehicle and employers’ liability insurance. This broad-based increase matters because it affects everyday life and business operations, not just rare catastrophic events. When several forms of cover rise at once, households and employers may be forced to make trade-offs—reducing coverage, accepting higher excesses, or dropping insurance altogether.

From a community perspective, the risk is cumulative. A household facing higher home insurance premiums may also be dealing with increased vehicle costs, while a local business may face higher liability cover. Over time, these pressures can weaken the ability of entire regions to recover from shocks.

Profitability and growth alongside unaffordability

One of the most contentious aspects of today’s debate is that rising premiums do not necessarily coincide with insurers struggling. Many insurers are reporting healthy profits, and globally the sector is experiencing “exceptionally strong growth.” Over the three years to 2024, revenue from premiums increased by more than 21% worldwide—a rise described as “whopping” by the finance corporation Allianz.

This juxtaposition—strong sector growth alongside growing unaffordability for customers—fuels political and public anger. It also complicates simplistic narratives that frame the issue solely as insurers being unable to cope. The sector may continue to grow and profit “until it no longer can due to climate change and other pressures.” But the argument emerging from the flood experience in NSW is that the more urgent concern is not a future crash of insurers. It is what happens to people and places as insurance protection retreats in the present.

Resilience is increasingly pushed onto households and communities

As insurance becomes harder to access or afford, the responsibility for coping is increasingly shifting away from institutions and onto individuals and communities. In the wake of major disasters, people do what they can to adapt, often in ways that reveal the limits of existing systems.

Examples cited in the current discussion include squatters taking possession of flood-damaged vacant homes in Lismore. Combined with the housing crisis, there is also mention of the growth in informal housing and settlements on the fringes of major population centres. These are described as desperate responses—but also as realistic ones when governments and insurers fail to reverse the trend of collapsing affordability and availability.

These developments show that insurance is not an isolated financial product. It is tied to housing stability, community cohesion, and the capacity to recover after disaster. When formal mechanisms fail, informal and precarious arrangements can expand, bringing new risks and vulnerabilities.

After each disaster: higher prices, less coverage

A recurring pattern is highlighted: after each major disaster event comes a rise in insurance costs and a withdrawal of insurance coverage. This dynamic can create a feedback loop. Disasters generate losses, losses push up premiums and tighten underwriting, and higher premiums or reduced coverage leave more people exposed when the next disaster hits. Over time, that cycle can turn a hazard-prone region into a place where living and doing business becomes financially untenable for those without substantial resources.

In this context, calls to “put the heat” on insurers, while politically resonant, may not address the deeper mechanics driving the retreat of affordable cover—especially when global reinsurance markets and concentrated market power are central to pricing and risk allocation.

Industry proposals and the limits of a narrow focus

Insurers, led by the Insurance Council of Australia, are pushing for measures such as a Flood Defence Fund and for retrofitting homes for disaster resilience, funded by governments and households. On the surface, these ideas may seem logical: reducing physical risk should, in principle, reduce financial risk.

However, critics argue that such proposals can draw attention away from the fact that insurance remains a thriving industry, and away from the need for regulations and policies aimed at making insurance more affordable and effective for ordinary people. The concern is not that resilience measures are inherently wrong, but that they can become a substitute for confronting the affordability and access crisis directly—particularly if the costs are shifted onto households already under pressure.

The case for government intervention

Given Australia’s exposure to disasters and the pattern of rising premiums and shrinking coverage, the argument is made that urgent government intervention is needed in an industry described as very resistant to such intervention. The aim would be straightforward: to ensure everyone is adequately covered when disaster strikes.

One proposed pathway is an equitable and affordable public insurance scheme. The rationale is that if private markets cannot reliably deliver affordable, accessible coverage—especially as climate-related disasters intensify—then a public option could help maintain a baseline of protection for households and communities.

Such an approach would sit alongside, not necessarily replace, other measures. But the emphasis here is on coverage that is both available and affordable, rather than leaving increasing numbers of people to fend for themselves in a high-risk environment.

Insurance, inequality, and social cohesion

The unfolding insurance crisis is also framed as a question of inequality. As more Australians lose the ability to insure themselves, governments are urged to address the growing structural inequality that is undermining social cohesion and the capacity for collective resilience. When some households can absorb rising premiums and rebuild quickly while others cannot insure at all, disasters can accelerate social and economic divides.

Underinsurance is part of this picture. When payouts fall short of the true costs of rebuilding or replacing what was lost, households may be forced into debt, prolonged displacement, or compromised living conditions. Over time, this can entrench disadvantage, particularly in communities repeatedly hit by disasters.

What the NSW floods reveal

The NSW floods have again demonstrated how quickly a natural disaster becomes a housing, financial and social crisis. The numbers—thousands of claims and potentially 10,000 damaged or destroyed properties—capture scale, but the deeper story lies in the gaps: those without cover, those priced out, and those whose insurance is not enough.

At the same time, the broader global context—dozens of billion-dollar disasters in a single year and hundreds of billions in losses—shows why this is not a temporary disruption. It is a stress test of how modern societies distribute risk, and of whether the systems designed to provide security can keep pace with changing conditions.

If Australia is to avoid becoming a warning example, the challenge is not only to ensure claims are processed quickly after catastrophes, but to confront the ongoing erosion of insurability itself. That means grappling with the realities of reinsurance, market concentration, and the widening gap between a growing insurance sector and the shrinking ability of ordinary people to buy meaningful protection.